Danantara is being built as more than a passive holding vehicle. Launched in 2025, it consolidates major state enterprises under a centralized structure intended to coordinate capital allocation across strategic sectors. ASEAN Briefing says the companies brought under the platform represent more than US$900 billion in state assets, while Reuters describes the mandate as managing about US$900 billion across 1,000 companies and using dividends to maximize investment returns. The portfolio spans banking, energy, telecommunications, infrastructure, and mining, setting up a state-backed capital allocator with reach across the economy.

A key plank is restructuring the SOE ecosystem. ASEAN Briefing notes that hundreds of SOEs and subsidiaries operate with overlapping mandates and uneven performance, and that policymakers aim to reduce the number of entities to around 200 companies through mergers, divestments, and sector-based holding structures. Lundgreen’s Investor Insights frames this as an attempt to reduce fiscal “bleeding” from underperformers and reallocate capital toward better-performing businesses. In practice, this consolidation can also change how private and foreign partners engage, because Danantara may become the central institutional counterpart for SOE-linked deals.

Downstreaming Turns Industrial Policy Into a Capital Allocation Test

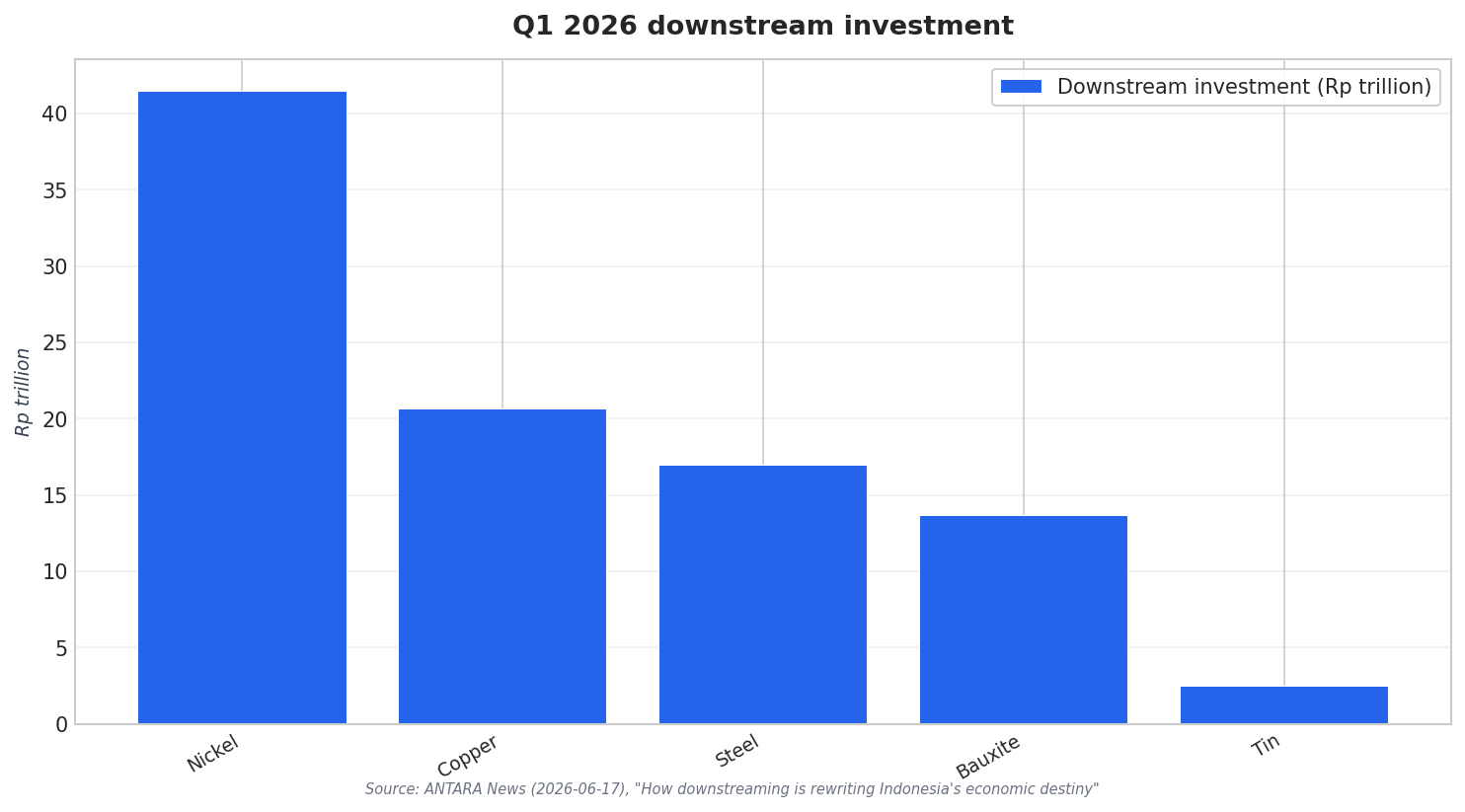

Indonesia’s downstreaming push is generating concrete investment flows that help explain why Danantara is being pulled deeper into industrial strategy. ANTARA reports realized downstream investment of Rp147.5 trillion (US$9.3 billion) in the first three months of 2026, equal to 29.6 percent of Indonesia’s total national investment of Rp498.8 trillion (US$31.5 billion) for the quarter. Minerals dominated the downstream pool at Rp98.3 trillion (US$6.2 billion), or roughly 67 percent. Nickel led at Rp41.5 trillion (US$2.62 billion), followed by copper at Rp20.7 trillion (US$1.31 billion), steel at Rp17 trillion (US$1.07 billion), bauxite at Rp13.7 trillion (US$865 million), and tin at Rp2.5 trillion (US$158 million).

Against that backdrop, Danantara’s investment program is increasingly read as downstreaming finance, not just portfolio management. Reuters quotes economists writing in the Bulletin of Indonesian Economic Studies who describe Danantara as “at once a sovereign wealth fund, a development bank and a public service provider.” Asia Times argues the fund is embedded in state-led industrial strategy, particularly downstreaming and resource nationalism, rather than operating at arm’s length from government. Bloomberg also reported Danantara’s interest in “Patriot bonds” to finance projects with social benefits. Taken together, the playbook blends returns with policy delivery, and that blend is becoming a defining feature of the Danantara Indonesia investment strategy.

The funding channels and project pipeline underline the scale of ambition. Reuters said a Danantara unit raised US$1.5 billion in its debut U.S. dollar bond sale, and that the sale was oversubscribed, which the fund said reflected strong investor confidence. Lundgreen’s Investor Insights adds that 18 projects prioritized under Danantara are cumulatively worth IDR 168 trillion (USD 37 billion), with about half allotted for mineral and coal projects. On energy, it cites nearly USD 14 billion for energy resilience and USD 2.36 billion for energy transition, and notes a partnership with Saudi-based ACWA Power with a potential value of USD 10 billion intended to attract more foreign capital into green energy.

How is Danantara changing Indonesia’s approach to managing SOEs?

What does the data show about downstreaming investment in early 2026?

Which downstreaming commodities attracted the most investment in Q1 2026?

How do analysts characterize the Danantara Indonesia investment strategy today?

What financing signals has Danantara shown to markets?