Indonesia’s VAT reform is not only a compliance issue. It is a pricing and margin problem that shows up in day-to-day decisions. Multiple sources link the VAT rate change from 11% to 12% to reform under Law Number 7 of 2021 on the Harmonization of Tax Regulations (UU HPP / HPP Law), with the increase taking effect no later than 1 January 2025. Businesses then have to translate the headline rate into what customers actually see, because some supplies can be exempt, zero-rated, or subject to government-borne VAT or reduced taxable bases. That design matters for consumer reactions. One practical account describes a CFO at a mid-sized fashion chain in Surabaya who feared that even a small visible increase would push customers to online rivals, so the company mapped which items carried the full burden and raised prices only on premium lines while seeking supplier discounts and tightening stock planning.

For pricing teams, the immediate question is how much of the tax becomes shelf price versus being absorbed. A key warning from a business-focused advisory source is that a 12% VAT environment can hurt margins if companies focus only on output tax while ignoring input credits. That framing turns VAT from a “rate change” into a working-capital and process issue, especially where import VAT, documentation, and cash flow management are involved. The same source argues that aligning Incoterms, supply chain routes, and warehouse locations helps manage VAT cash flow and duties, so landed costs stay competitive in regional markets. In other words, the pricing strategy is inseparable from how transactions are structured, invoiced, discounted, and classified across the supply chain.

Why the 12% Rate Does Not Hit Every Basket the Same Way

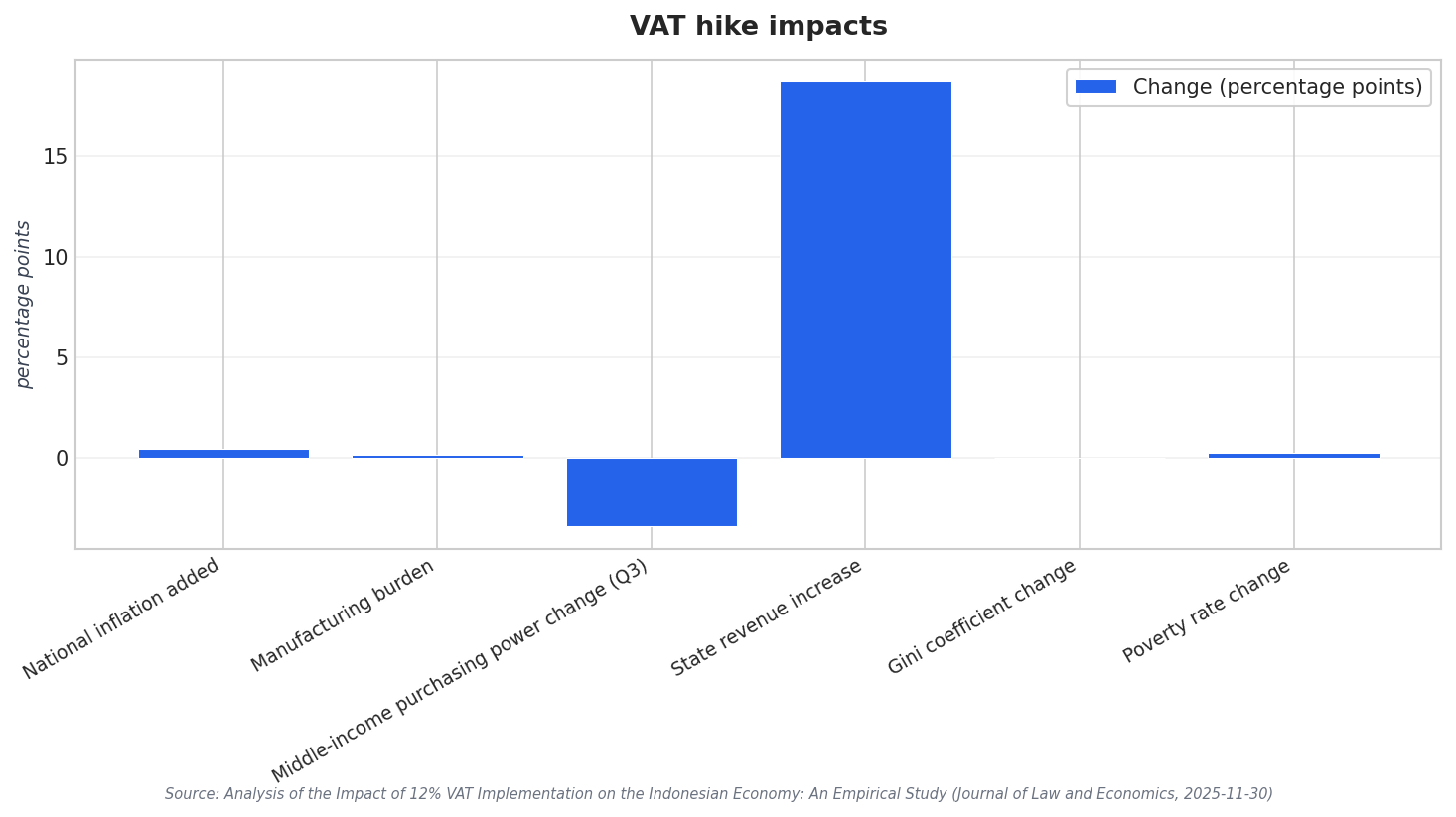

The Indonesian VAT story is also about uneven household impacts. An empirical study covering January–June 2025 used a Difference-in-Differences (DiD) approach with time series data from Statistics Indonesia (BPS), Bank Indonesia, and the Ministry of Finance, alongside household surveys and MSME data. It found the 12% VAT added 0.45 percentage points to national inflation, with manufacturing bearing the largest burden at 0.18 percentage points. The same study reported a U-shaped pattern in purchasing power effects: middle-income groups (quintile 3) saw the steepest decline of 3.4%, while low- and high-income groups experienced smaller reductions. It also described regressive characteristics, with the Gini coefficient moving from 0.381 to 0.394, poverty rates rising from 9.54% to 9.78%, and approximately 640,000 people pushed below the poverty line.

Those distributional effects shape where consumer spending may soften and where businesses may need to rethink product mixes. One advisory interpretation is that the headline 12% rate is focused more on discretionary and luxury consumption, while essential goods are generally protected through exemptions, zero-rating, government-borne VAT, or reduced taxable bases that keep many essential items closer to an effective 11% load. From a legal and technical standpoint, VAT is regulated under Law Number 8 of 1983 as amended, with the HPP Law guiding rate adjustments, and further implemented through Government and Minister of Finance regulations. PMK 131/2024 is cited as a fairness-oriented measure that differentiates the application of the 12% rate and the tax base (DPP) depending on the type of goods or services, including luxury goods where VAT is calculated by applying 12% to the DPP in the form of selling price or import value.

For executives tracking the Indonesia VAT increase impact, the practical takeaway is to model margin and demand together, product by product. The same January–June 2025 study reported state revenue increased by 18.7% and noted mitigation interventions worth 0.3–0.5% of GDP became necessary, underscoring that policy gains can coexist with household strain. On the business side, sources emphasize correct classification of supplies, including identifying what is fully taxable versus exempt, zero-rated, or outside VAT, such as certain employee benefits or purely financial transactions. That classification, plus disciplined use of input credits and supply chain planning, can be the difference between a manageable price change and silently absorbing tax costs through reduced margins.

When did Indonesia’s VAT rate increase from 11% to 12% take effect?

What did research find about inflation after the 12% VAT implementation?

How did purchasing power change across income groups?

What does the Indonesia VAT increase impact mean for pricing and margins?

What poverty and inequality changes were associated with the VAT increase in one study?