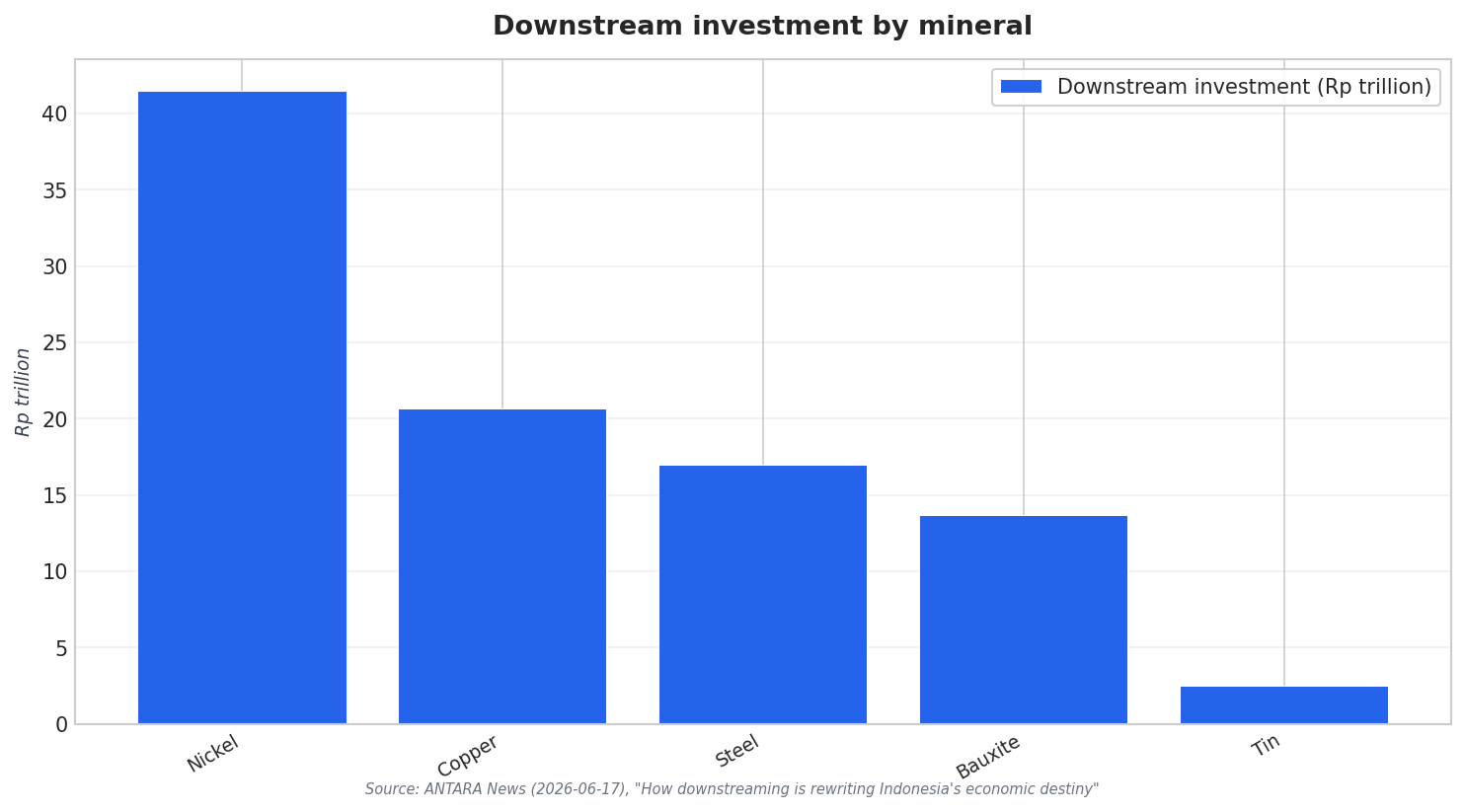

Indonesia’s push to process more minerals at home is reshaping where capital goes and what kinds of projects can scale. One snapshot comes from ANTARA’s reporting on downstream investment: the mineral sector commanded Rp98.3 trillion (US$6.2 billion), or roughly 67% of the total downstream pool. Within that mineral allocation, nickel led at Rp41.5 trillion (US$2.62 billion), while copper reached Rp20.7 trillion (US$1.31 billion), bauxite Rp13.7 trillion (US$865 million), and tin Rp2.5 trillion (US$158 million). The same source notes that around 75% of downstream investment is now located outside Java, signaling that mineral-producing provinces are becoming the primary hosts for new industrial activity and related services.

Copper stands out because it combines investment momentum with documented market scale. Grand View Research estimates Indonesia’s copper mining market generated revenue of USD 4,552.1 million in 2022 and is expected to reach USD 4,644.1 million by 2030, implying a CAGR of 0.3% from 2023 to 2030. Indonesia also represented 2.5% of the global copper mining market in 2022. Demand-side positioning matters for planning processing and domestic offtake: in 2022, building & construction was the largest end use segment, with a revenue share of 40.35%, while machinery & equipment is identified as the most lucrative end use segment with the fastest growth during the forecast period.

Roadmap Signals by Mineral: What the Numbers Suggest

Exploration and operational performance indicators add more texture to Indonesia’s copper opportunity set. S&P Global reports that in 2024 Indonesia’s exploration budget totaled $113.8 million, representing 35% of the Pacific-Southeast Asia region’s allocation. Within that budget, gold took 58% and copper 24%, while minesite exploration rose to 71% in 2024 from 52% in 2023. S&P Global also flags the emissions dimension: Indonesia’s average emission intensity on its 2024 copper emissions curve is 2,535 kg CO2e/t Cu, above the global average of 2,495 kg CO2e/t Cu, and by 2030 Indonesia’s average copper mine emission is expected to drop 21% from 2021 levels as the power mix shifts toward natural gas, hydro, and renewables.

Bauxite downstreaming is framed in policy-and-demand terms in IndexBox’s industrial minerals coverage. It describes a “state-mandated creation of downstream metal processing industries,” and says a similar policy for bauxite is fostering the development of alumina refineries, shifting demand away from export markets toward domestic processing facilities. This intersects with the investment ranking reported by ANTARA, where bauxite drew Rp13.7 trillion (US$865 million) within the downstream mineral pool. The same ANTARA report points to institutional anchors within the MIND ID Group portfolio, noting ANTAM’s role across nickel and bauxite value chains. Together, these signals suggest the roadmap’s practical center of gravity is not only mining, but also where refineries, logistics, and compliance-ready operations can meet downstream obligations.

Tin is a different kind of downstream story: it mixes established industry structure with uneven market expectations. ANTARA reports downstream investment of Rp2.5 trillion (US$158 million) associated with tin. Grand View Research estimates Indonesia’s tin mining market generated USD 1,694.8 million in revenue in 2022 and anticipates a CAGR of -1.9% from 2023 to 2030. Segment detail still indicates where product strategies may concentrate: solders were the largest segment in 2022, while batteries are cited as the most lucrative product segment registering the fastest growth during the forecast period. In practice, the Indonesia mineral downstreaming agenda in tin will likely reward players that can align product mix, efficiency, and environmental management with stricter expectations while staying competitive through cycles.

How large is the downstream investment pool for minerals, and where do copper, bauxite, and tin rank?

What do current market outlooks say about Indonesia’s copper mining revenues?

What exploration signals support Indonesia’s copper opportunity pipeline?

How is bauxite policy expected to change demand patterns in Indonesia?

What is the outlook for tin, and which segments stand out?